Unified Pension Scheme (UPS) announced by the central government for its employees and as an option for state governments has been in news a lot. It’s a departure from the National Pension System, announced with much fanfare and rare political consensus, in 2004 by then Prime Minister Atal Bihari Vajpayee and was strengthened further by Prime Minister Manmohan Singh. Result was that National Pension System (NPS) from its humble beginnings in 2004, with almost zero distribution incentive and negligible marketing from anyone has gone onto become a 12lac crore behemoth. It became the favoured long-term savings instrument of government with NPS specific tax rebates under section 80CCD (1) (tax rebate for individuals contributing up to 50,000) and 80CCD (2) (Up to 14% of basic + DA contributed by employer) made tax free.

Pension Scheme If the NPS was so good then what forced the government to backtrack? The answer lies in allure of guaranteed income and the nature of democracy where any organised micro minority, in this case government servants, can sway the resources towards itself. This last point is particularly important for NPS subscribers because, in time, they will also become a big group. Whether they can be organised is something that remains to be seen.

Why was NPS set up? Because pension bill of govt is out of hand!

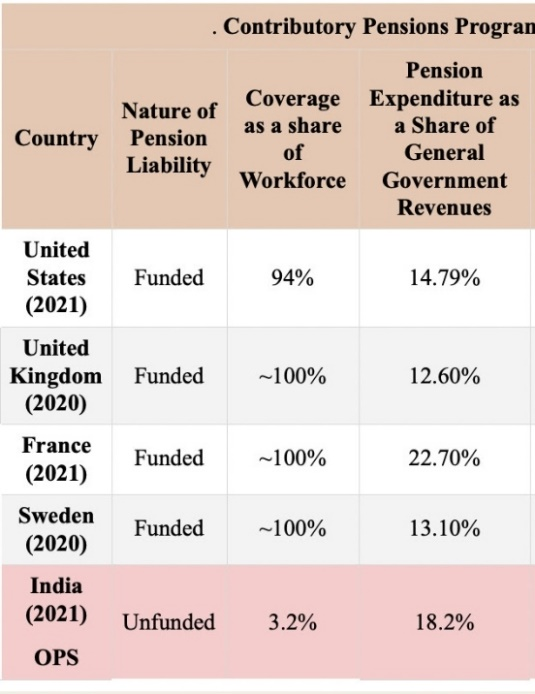

Old Age income security for government servants is a good idea. But sometimes good ideas carry on too far and become a problem. That is precisely what happened to government employee pensions. And there is history to it. British Govt, when they were ruling India, had some of the best employee benefits in the world. And that was natural since they were a colonial power. They had had to buy their employees loyalties and hence the over generous pay and pensions. After the British left there should have been reforms in civil services to make them more suited to new realties of India. However, for a number of reasons, that has not happened fully yet. So, it was no surprise that the pension arrangement of British continued even after independence. This resulted in a heavily lopsided system which is captured in the adjoining graph.

You will notice that while the developed countries like United States, UK and France cover nearly 100 % of their work force with 15-20% of government revenue going towards funding these pension liabilities, India covers only 3.2% of its workforce for pensions and spends 18% of government revenues dedicated towards welfare of this section. And almost all of this 3% are government employees. This kind of expense on social security of a very small and higher paid section of workforce which enjoys many other perks like job security, subsidised housing, fully paid health care etc was what would have seemed odd to Prime Minister Vajpayee and Manmohan Singh.

Apart from the morality of government employees getting so much more than private citizens, there was an economic factor. Pension is a complex thing to manage. World over, governments and companies run pensions by creating a savings pool in which employees and employers contribute throughout their working lives. This pool is managed by professional investment experts and the funds’ ability to pay pensions is closely monitored by technical valuation by actuaries. This creates a funded pension system which is sustainable. This is the reason why you see retirement ages being increased across Europe to make sure the pensions remain viable. Indian pension system however had none of these features. The pensions were funded from the state exchequer. Hence as the pension bills increased, governments had less to spend on health, education and other social sector measures.

Enter the NPS: The UPI equivalent of pension systems

To mitigate these issues government set up the National Pension System, initially for only government employees but was later opened up for the private citizens. UPI is a payment solution built in India for the world. National Pension System should qualify for the same tag in context of pensions

1. The selling commission of NPS was kept very low to eliminate the chances of missell. This did hurt the initial adoption rate but as the inherent strength and quality of NPS became widely known customers themselves started asking for it. NPS is perhaps the only financial product that can justifiable call itself a pull product.

2. NPS fund management fees are 0.01% of funds. This is the lowest in the world. To put it in perspective, a direct mutual fund charging 1.25% would be 125 times more expensive than NPS! When you put this against the corpus size of 12lac crore, this year’s NPS subscribers have saved 12,000crore in fund management charges.

3. NPS has an open architecture. The seller, customer servicing and fund management are all separate entities with specific roles. They are not allowed to do anything else except their core job. This cuts out the incentive to missell.

4. The customer can shift sellers, customer service and fund manager seamlessly without any administrative hassle. Same holds true even for employers. Unlike PF where the registration number changed every time the employer changed, in NPS the customer has a permanent account number.

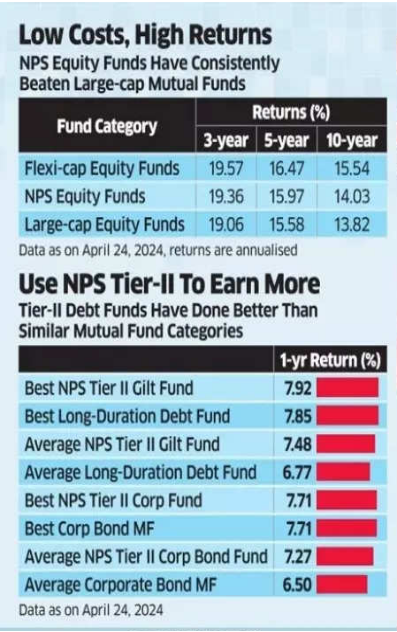

5. The returns for NPS, as the infographic shows, were no less than Mutual Funds. NPS funds actually beat majority of the large cap Mutual Funds over the last 10 years.

If NPS was good, Why is Unified Pension Scheme needed?

Basis the performance of NPS funds and generous contribution from government (14% of salary) and from employee (10% of salary) the resultant corpus would provide for comfortable retirement for the government employees. It would also not place undue burden on the economy of country and free up resources to focus on education, infrastructure and health. NPS would give a comfortable pension but not luxury of guaranteed 50% of last drawn salary along with periodic increase in line with salary increase of government employees.

From 2004 to 2014 both Congress and BJP governments supported National Pension System. Without going into partisan politics, a particular political party attempted to buy votes of the roughly 1.4 cr government employees and their families by promising return to old pension system. And given the nature of politics in the country the ruling party, after resisting for a few years, has had to finally give up and concede the demand. So now the servants of public can get pensions that public can only dream of.Unified Pension Scheme: Mix of NPS and Old Pension scheme

Under UPS the government has accepted to give a guarantee of 50% of last drawn salary to government employees after completion of 25 years of government service. However, in departure from old pension scheme where pension was paid from government revenue account, in effect passing on the load of pension completely to future generations, the government has retained the contributory nature of NPS. This means that 28% of the salary of the employee (10% by employee and 18% by the government) will be put into a fund, managed by NPS fund managers, and employees’ pension will be paid out of this fund. In case the collected corpus is not sufficient to make the guaranteed payment government will chip in to make up the difference. There will be regular actuarial valuation to asses the asset liability matching.

This transparency is a ray of hope. Since the governments will have to start saving for the pensions today as opposed to current pensions where one could win elections by making unsustainable promises today and passing on the financial crisis to future generations, the cost of government pensions will become visible to increasingly educated citizens who will then want to question the level of government expenditure. This will, in my opinion, result in smaller number of government servants in the future with most jobs getting outsourced. Have you noticed the private sector guards managing airport check-ins in last few years? That in the long run might be the best thing to happen to the country.

Incidentally Himachal Pradesh government, which won the election on promise to restore old pension plan, in less than two years has reportedly run out of money to pay current salaries. This is not to suggest that old pension scheme alone is responsible for the mess.

Conclusion

Secure is designed to provide you and your family with comprehensive, accessible, and affordable healthcare solutions. Whether you’re an individual, a family, or a senior citizen, there’s a plan designed to provide financial security and peace of mind.

Some key reasons why you should choose CarePal Secure are:

Extensive Coverage: Get access to a wide network of hospitals for cashless treatments, covering everything from regular health check-ups to major hospitalisations.

No Waiting Period for Essential Coverage: CarePal Secure offers immediate access to essential healthcare benefits so that yCarePal ou can receive critical medical treatment without long approval delays.

24/7 Medical Assistance & Claims Support: Our dedicated helpdesk is available round-the-clock to assist you with medical emergencies, claim processing, and consultation bookings.

Teleconsultations & Healthcare Discounts: Our seamless teleconsultation services allow you to access specialists across 18+ medical fields. Additionally, you can enjoy significant savings on medicines, diagnostic tests, and outpatient care, making quality healthcare more affordable.

Affordable Plans with Super Top-Up Options: Choose from a range of budget-friendly plans for individuals, families, and seniors. Our super top-up policy for seniors provides additional financial protection, covering larger medical expenses at a lower cost.

Tax Benefits Under Section 80D: The premiums paid toward CarePal Secure health insurance are tax-deductible, helping you save money while ensuring comprehensive coverage for yourself and your family.

With trusted partners nationwide, CarePal Secure ensures that quality healthcare is always within reach. So what are you waiting for? Join 80,000+ satisfied customers who trust CarePal Secure for their healthcare needs.

Get in touch with us to know the right plan for you.