Health insurance cost is a vital aspect of financial planning and healthcare management. It provides individuals and families with a safety net, ensuring medical expenses do not lead to financial distress.

In India, where healthcare costs are rising steadily, having adequate health insurance is becoming increasingly important. This blog aims to delve into the complexities of health insurance costs in India, providing a comprehensive understanding of what to expect and how to make informed decisions.

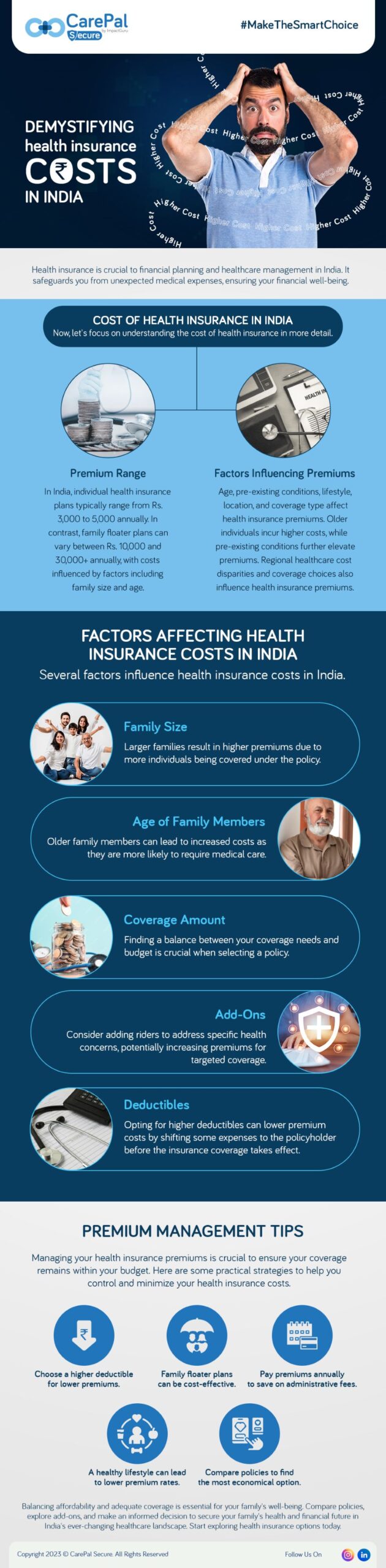

Cost Of Health Insurance In India

Understanding health insurance costs in India is crucial due to many factors. Let’s explore the details of health insurance expenses in this diverse context.

- Premium Range: Health insurance premiums can vary significantly in India. On average, an individual health insurance plan can start at around Rs. 3,000 to Rs. 5,000 per year for basic coverage. Family floater plans, covering the entire family, can range from Rs. 10,000 to Rs. 30,000 or more per year, depending on factors like family size and age.

- Factors Influencing Premiums: The cost of health insurance premiums is influenced by several key factors. Your age plays a significant role, with older individuals generally facing higher premiums due to increased health risks. Pre-existing medical conditions can also raise costs as they require more extensive coverage. Lifestyle choices, such as smoking, contribute to higher premiums. Geographic location impacts pricing due to regional healthcare cost variations. Additionally, the specific type of coverage you choose, be it basic or comprehensive, directly affects your premium rates.

Factors Affecting Health Insurance Costs In India

Understanding the intricacies of health insurance costs in India is crucial for making informed decisions about your healthcare coverage. To delve deeper into this topic, let’s expand on the factors that influence health insurance costs:

Premiums: The premium is like the heartbeat of an insurance policy. It’s the amount you pay the insurance company to maintain your coverage. The premium varies based on several key factors, each of which deserves a closer look:

- Age: Your age is a fundamental determinant of your health insurance premium. Younger individuals generally pay lower premiums because they are considered to be at a lower risk of developing severe health conditions. As you age, the likelihood of health issues increases, and so does your premium.

- Health Condition: Your current health status can significantly impact your premium. Individuals with pre-existing medical conditions may face higher premiums. Insurers assess the risk associated with your health, and those with a clean bill of health typically enjoy lower premiums.

- Sum Insured: The sum insured, also known as the coverage amount, is the maximum amount the insurance company will pay for your medical expenses. Opting for a higher sum insured results in a higher premium. It’s essential to balance adequate coverage and affordability when selecting this amount.

Policy Type: Health insurance plans in India come in various types, catering to different needs and preferences:

- Individual Plans: These policies cover only one person, making them ideal for individuals who want personalized coverage. Premiums for individual plans are typically lower compared to family plans.

- Family Floater Plans: Family floater plans are designed to cover the entire family under a single policy. They are usually more cost-effective for families as the premium is calculated based on the age and sum insured for the primary insured member. Other family members, such as spouses, children, or parents, are covered under the same premium.

- Group Policies: Group health insurance policies are provided by employers or organizations for their employees. These policies often have lower premiums due to group buying power and are a valuable employee benefit.

Add-Ons and Riders: Health insurance policies can be customized to meet specific needs by adding riders or add-ons. While these extras come at an additional cost, they can be invaluable in certain situations.

- Critical Illness Rider: This rider provides a lump-sum payout if you are diagnosed with a critical illness such as cancer or heart disease. It can help cover additional expenses not included in a standard policy.

- Maternity Benefits Rider: For expecting parents, this rider covers maternity-related expenses, including childbirth and pre/postnatal care.

- Hospital Cash Rider: It offers a daily cash benefit for each day you spend in the hospital, helping to cover incidental expenses during your hospital stay.

Did You Know?: Adding riders to your policy can be a cost-effective way to enhance your coverage tailored to your needs. However, carefully assess your requirements and budget before adding riders, as they increase the premium.

Network Hospitals: Many insurance companies in India have tie-ups with a network of hospitals. Seeking treatment at these network hospitals can have financial benefits for policyholders. You can avail of cashless services, where the insurer settles the bill directly with the hospital, saving you from the hassle of reimbursement procedures.

Fact: In India, the Insurance Regulatory and Development Authority of India (IRDAI) regularly monitors and regulates health insurance premiums. This ensures that premiums are reasonable and fair, preventing insurers from charging exorbitant amounts.

In summary, the cost of health insurance in India is influenced by many factors, including age, health condition, policy type, add-ons, network hospitals, and the sum insured. To make an informed decision, it’s essential to carefully assess your specific requirements and budget constraints, compare policies from multiple insurers, and seek professional guidance if needed.

By understanding these factors, you can easily find affordable health insurance in India with suitable coverage.

How Much Should Family Health Insurance Cost?

Family health insurance is a practical and cost-effective approach to prioritizing your loved ones’ well-being while safeguarding your financial stability. To determine the appropriate cost, consider the following factors:

Family Size: The number of family members you intend to include in your policy is a fundamental factor that directly influences the cost. Naturally, a larger family necessitates a higher sum insured, which, in turn, leads to a proportionally higher premium. When deciding on family size for insurance coverage, consider present and any potential additions to your family.

Age of Family Members: The age of each family member plays a significant role in shaping the cost of your family health insurance. Older family members tend to be associated with higher health risks, which insurance companies consider when determining premiums.

Coverage Amount: Selecting the appropriate coverage amount is pivotal in balancing your family’s medical needs with your budget. While a larger sum insured results in a higher premium, it also ensures comprehensive protection for your family in the event of unexpected medical expenses. It’s essential to strike a balance between adequate coverage and affordability.

Add-ons: To tailor your family health insurance plan to the specific health concerns within your family, consider incorporating add-ons or riders. These additional features can extend coverage for critical illnesses, maternity benefits, or other unique needs. Although these enhancements come at an extra cost, they provide invaluable peace of mind and comprehensive coverage.

Deductibles: Some insurance policies offer deductibles, which are predetermined amounts you agree to pay from your own pocket before the insurance coverage occurs. Opting for a higher deductible can lower your premium, making health insurance more affordable. However, assessing your financial capacity is essential to covering the deductible in case of a medical emergency.

Network Hospitals: Investigate whether your chosen insurer has established partnerships with a network of hospitals in your locality. This can be particularly advantageous, as it often leads to substantial cost savings on hospitalization expenses. The added convenience of cashless services offered by network hospitals further enhances the value of such partnerships.

Given these factors, it’s crucial to recognize that the typical family size in India, as reported by the Insurance Regulatory and Development Authority of India (IRDAI), usually falls within the range of 4 to 5 members. Hence, when considering family health insurance, a prudent starting point for selecting the sum insured generally lies between Rs. 5 lakhs and Rs. 10 lakhs.

But here’s an interesting fact: CarePal Secure offers a comprehensive plan that ensures year-round coverage for up to four family members. With our comprehensive coverage, including discounts on medicines, OPD coverage, teleconsultations, and a 24×7 claim helpdesk, you can safeguard your family’s well-being during medical emergencies. We are dedicated to providing year-round peace of mind through our comprehensive plans, ensuring your loved ones’ security.

Effective Premium Management Tips For Health Insurance

While health insurance premiums tend to rise annually, you can adopt strategies to manage your premiums and keep them within your budget effectively:

- Opt for a higher deductible: Selecting a policy with a higher deductible implies that you will pay more from your pocket before your insurance coverage begins. However, this choice often leads to reduced premium costs.

- Choose a family floater plan: Family floater plans encompass multiple family members under one policy, often proving more cost-effective than individual policies for each member.

- Pay premiums annually: Opting for annual premium payments instead of monthly installments can lead to savings, as it typically reduces administrative fees.

- Embrace a healthy lifestyle: Maintaining a healthy lifestyle by exercising regularly and refraining from smoking can contribute to lower premium rates, as insurers often reward healthy behaviours.

- Compare policies: To find the most economical option tailored to your requirements, compare health insurance policies from various providers. This step can help you identify the best-suited policy for your financial needs.

In conclusion, the cost of health insurance in India is influenced by various factors, including age, family size, coverage amount, and the type of policy you choose. It’s crucial to balance affordability and adequate coverage to ensure your family’s well-being.

Remember to compare policies, read the fine print, and consider add-ons that align with your family’s specific needs. By making an informed decision, you can secure your family’s health and financial future in an ever-changing healthcare landscape. Don’t wait—start exploring health insurance options today to safeguard your family’s future.

Conclusion

Secure is designed to provide you and your family with comprehensive, accessible, and affordable healthcare solutions. Whether you’re an individual, a family, or a senior citizen, there’s a plan designed to provide financial security and peace of mind.

Some key reasons why you should choose CarePal Secure are:

Extensive Coverage: Get access to a wide network of hospitals for cashless treatments, covering everything from regular health check-ups to major hospitalisations.

No Waiting Period for Essential Coverage: CarePal Secure offers immediate access to essential healthcare benefits so that yCarePal ou can receive critical medical treatment without long approval delays.

24/7 Medical Assistance & Claims Support: Our dedicated helpdesk is available round-the-clock to assist you with medical emergencies, claim processing, and consultation bookings.

Teleconsultations & Healthcare Discounts: Our seamless teleconsultation services allow you to access specialists across 18+ medical fields. Additionally, you can enjoy significant savings on medicines, diagnostic tests, and outpatient care, making quality healthcare more affordable.

Affordable Plans with Super Top-Up Options: Choose from a range of budget-friendly plans for individuals, families, and seniors. Our super top-up policy for seniors provides additional financial protection, covering larger medical expenses at a lower cost.

Tax Benefits Under Section 80D: The premiums paid toward CarePal Secure health insurance are tax-deductible, helping you save money while ensuring comprehensive coverage for yourself and your family.

With trusted partners nationwide, CarePal Secure ensures that quality healthcare is always within reach. So what are you waiting for? Join 80,000+ satisfied customers who trust CarePal Secure for their healthcare needs.

Get in touch with us to know the right plan for you.